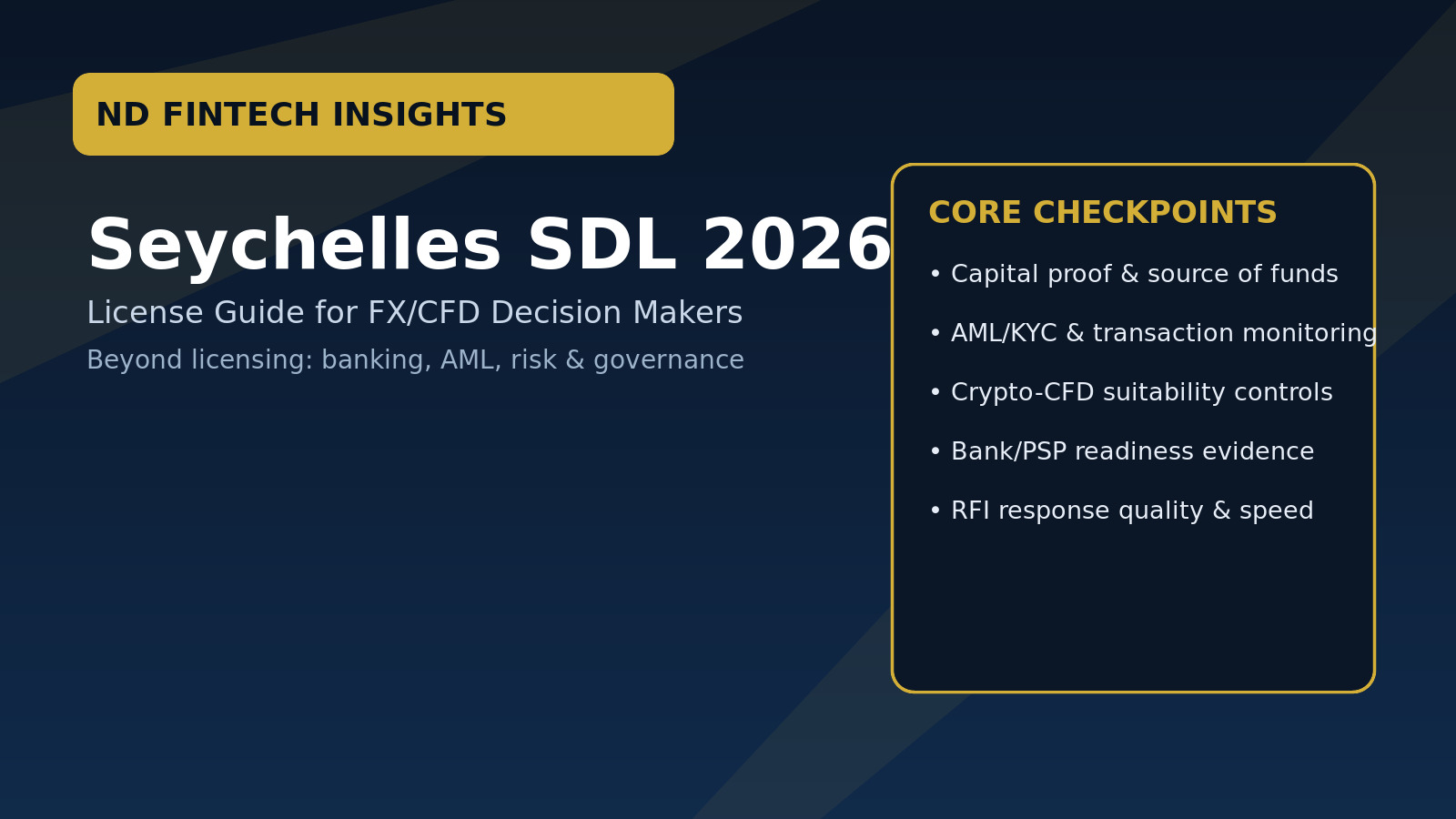

2026 Seychelles SDL Guide: The Real Barrier Is Banking, Compliance, and Risk Execution

Author: OPAL

Author: OPALThe value of Seychelles SDL is not just licensing. Execution quality in AML/KYC, bank readiness, source-of-funds evidence, and risk governance is what determines success.

Many teams simplify the Seychelles Securities Dealer License (SDL) as just a “forex license.” In practice, that misses the real point. In 2026, SDL is valuable because it can support a multi-asset model — but only if your operating controls are real, auditable, and bank-ready.

If AML/KYC, source-of-funds, risk controls, and governance exist only on paper, the project usually gets blocked later by banks, PSP due diligence, LP onboarding, or regulator RFIs.

This guide is written for FX/CFD decision makers who need execution clarity, not marketing language.

1) What SDL is and what it can cover

Seychelles SDL is issued by the Financial Services Authority (FSA) under the Securities Act 2007. It is commonly used for:

- Forex brokerage

- CFD products (FX, commodities, indices, equities)

- Leveraged derivative products (subject to model)

- Crypto-CFD product lines

ND FINTECH view: SDL is suitable for operators building an actual multi-asset platform. If you only need a light referral/IB structure, SDL may be an inefficient cost profile.

2) Why SDL is still relevant in 2026

Broad product scope in one framework

A wider licensed scope improves your ability to negotiate with banks, PSPs, LPs, and infrastructure partners.

Capital requirement is manageable — but must be provable

A commonly referenced threshold is USD 100,000. The real challenge is proving source of funds and maintaining a verifiable evidence trail.

Structure and tax planning require group-level design

Do not evaluate SDL using only a headline tax number. You must align entity substance, treasury flow, cost centers, and cross-border operating logic.

Foreign ownership flexibility

For international founders, SDL structures can be useful for ownership planning and scale preparation.

3) Crypto-CFD: clear signal, high execution bar

Interest in SDL often comes from teams planning Crypto-CFD, not spot exchange.

A clearer regulatory signal is helpful, but success still depends on operational depth:

- Suitability testing process

- Risk disclosures and leverage controls

- Data retention and audit traceability

Banks and PSPs approve operations, not slide decks.

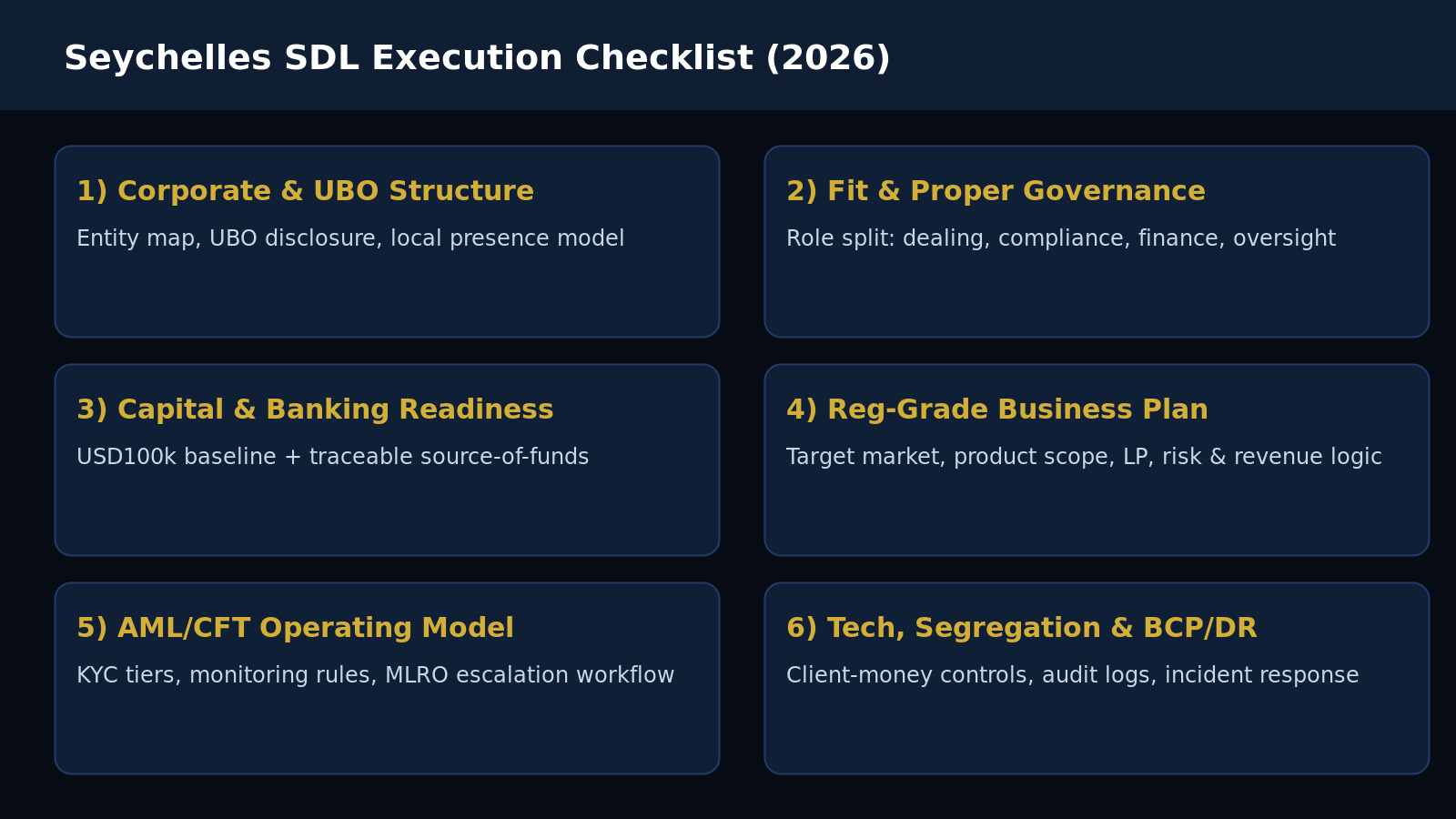

4) SDL application is a systems project, not a document project

Use this 7-block execution checklist:

- Corporate structure and UBO clarity

- Fit & Proper governance with role separation

- Capital proof and source-of-funds evidence chain

- Business plan that survives regulator Q&A

- AML/CFT controls with monitoring and escalation

- Operational infrastructure (segregation, security, BCP/DR)

- Outsourcing governance with internal accountable owner

5) Real timeline: where 8–12 months is usually spent

Most delays happen in:

- Bank onboarding and repeated KYC cycles

- Regulator RFI response quality/speed

- Inconsistency between submitted documentation and real operating model

6) Budgeting without underestimation

Plan in four layers:

- Annual regulatory fees

- One-off setup and application costs

- Ongoing compliance operations

- Audit and mandatory reporting

Hidden cost is usually not filing — it is bank and PSP readiness work.

7) Who should (and should not) choose SDL

Suitable if you:

- Operate or plan to operate FX/CFD multi-asset business

- Need market-recognized regulatory identity for LP/PSP/banking

- Are ready to implement compliance and risk as a running system

Not suitable if you:

- Only want the cheapest “license-looking” setup

- Are not ready for banking/payment due diligence

- Keep changing product, market, and fee model every month

Final takeaway

The real advantage of SDL is not license possession. It is operational credibility: whether your compliance, risk, and governance can be demonstrated, tested, and scaled in live operations.

When done correctly, SDL becomes a growth structure — not just a certificate.